An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. - Warren Buffett

Syndax Pharmaceuticals (NASDAQ:SNDX) is one of the new companies that we featured within the previous month. Interestingly, the firm recently reported the data for the ENCORE 601 trial. This is a sneak peek preview prior to the data to be presented at the American Society of Clinical Oncology (��ASCO��) Annual Meeting scheduled on June 1-5, 2018 in Chicago, Illinois.

Despite what was seemingly promising data, the market was not impressed and thus the stock tumbled significantly. The elephant in the room is where the shares are heading (and what investors can expect from Syndax). In this research, we��ll elucidate the recent clinical findings in its appropriate context to gauge where the shares are heading.

Figure 1: Syndax stock chart. (Source: StockCharts).

Fundamental Analysis

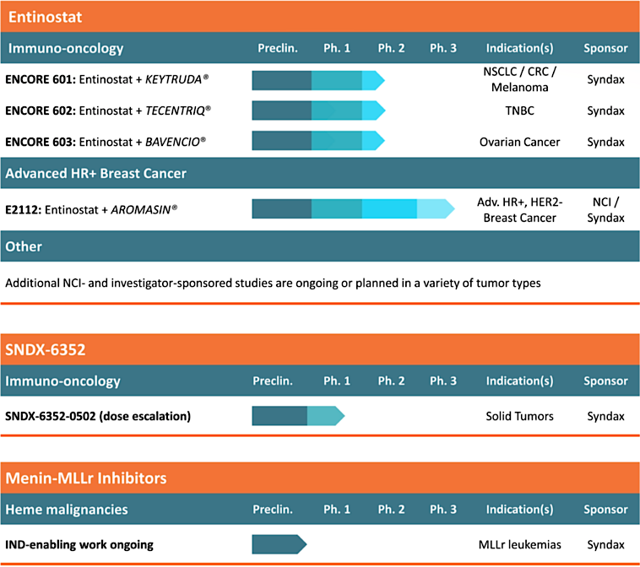

First things first, we wish to share an overview for new investors. Accordingly, Syndax Pharmaceuticals is headquartered in Waltham MA. The company is focusing on the therapeutic innovation and commercialization to service the oncology market. Leveraging on its immuno-oncology expertise, the firm is developing two potential best-in-class assets, entinostat and SNDX-6352 (as depicted in figure 2). For an in-depth discussion of the underlying science of entinostat and SND-6352, investors can refer to our initial analytical research on Syndax.

Figure 2: Therapeutic pipeline (Source: Syndax)

As alluded, Syndax reported the preliminary outcomes of the Phase 2 (ENCORE 601) trial on May 17, 2018. As a Phase 1B/2 trial investigating entinostat in combinations with pembrolizumab (Keytruda) of Merck (NYSE:MRK), ENCORE 601 is assessing the aforesaid combo regimen in multiple cohorts of PD-L1 treatment-naive and pre-treated cancers, including non-small cell lung cancer (��NSCLC��), melanoma, and microsatellite stable colorectal cancer (��MSS-CRC��).

At the time of interim analysis (i.e. data cut-off), there were six of 57 patients with NSCLC on the combination regimen who demonstrated partial responses for an 11% objective response rate (��ORR��). The median duration of response (��DOR��) was 4.6 months, with the longest observed response over 14 months. At cut-off, seven patients remain on study. Of note, these patients are extremely sick patients (with 22 or 38% cases already resistant to prior PD-L1 therapy); hence the ORR could not be as robust as what the market had expected. Commenting on the latest data development, the CEO (Dr. Morrison) remarked:

The additional data from the ENCORE 601 program continue to support the potential for the entinostat-pembrolizumab combination to serve as an effective therapeutic option across a variety of indications. We are especially pleased to be able to share preliminary findings from our efforts to identify biomarkers that could aid in predicting which patients may derive a clinical benefit from this combination therapy. We have now identified a potential registration pathway in NSCLC and look forward to providing further updates as our plans come together.

That aside, it��s interesting that the blood samples were collected and analyzed for 51 of the 57 NSCLC patients enrolled. Accordingly, the pre-treated baseline level of various markers was measured. One key assessment that stood out was the immune cells coined ��monocytes,�� which are immature macrophages - the immune cells that engulf pathogens and cancers. As follows, the early data explicated that patients with a higher level of monocytes (14 patients) demonstrated an elevated ORR of 29%, thereby representing 4 partial responders (��PR��) out of 14 patients as mentioned.

In addition, this subgroup remarkably showed the PFS of 5.4 months: this is much higher than the 2.8-month average for NSCLC managed with the 3rd-line chemotherapy (following progression after platinum doublet and PD-L1 treatment). The therapeutic effects of the combo drug are seemingly dependent on the monocytes level. As demonstrated in the patients with lower baseline levels of monocytes, the ORR was only 5% (2 PRs out of 37 patients) and the PFS was simply 2.5 months.

It is imperative to note that the overall patient population (n=57) achieved a PFS of 2.7 months, which is slightly lower than the aforesaid 2.8 mark. Therefore, it is unlikely that the entinostat-Keytruda will demonstrate key advantages over the 3rd-line regimen. Perhaps, the market was reacting negatively to this outcome. Be that as it may, the subpopulation is the key value driver of the NSCLC franchise. With 92% improvement over the standard 3rd-line chemotherapy, it��s most likely that this can be developed for the patients with a higher level of monocytes.

Based upon these findings, Syndax has identified a potential registration path in patients with NSCLC who have progressed on a PD-L1 inhibitor. The trial is expected to start by the end of 2018. Asides from Dr. Morrison, the Director of Thoracic Medicine Oncology Program at NYU Langone Perlmutter Cancer Center (Dr. Leena Gandhi) enthused:

NSCLC patients whose disease has progressed on PD-L1 and chemotherapy are in need of options that offer meaningful clinical benefits. Initial findings from this cohort of NSCLC patients receiving the entinostat-pembrolizumab combination provide encouraging benefit in ORR and PFS. Although more data is needed, promising results for a population of patients with high monocyte counts further highlight that a selection strategy may lead to enhanced benefits for patients.

Investors should be cognizant that while the strong results for the aforementioned combo franchise were not achieved for NSCLC in the overall patient population, it certainly did for the subcohort. Like cobimetinib of Exelixis (NASDAQ:EXEL) that did not procure strong clinical outcomes for the advanced colorectal cancer, nevertheless, it delivers robust results and is approved to treat resistant melanoma. The key point in the ENCORE 601 study is that it measures a vast number of biomarkers' assessment of pre- and on-treatment to better guide registration-directed studies that are most likely to bear fruits.

Final Remarks

Syndax is riding on the power of two lead molecules (entinostat and SNDX-6352) to power an enriched pipeline that can deliver hope to patients afflicted by various deadly cancers. If the reporting for the Phase 3 (E2112) within months turns out positive as we prognosticated, the share can appreciate by approximately one fold. Given the various partnership with Merck and Roche (OTCQX:RHHBY) for the co-development of entinostat with their flagship molecules (Keytruda, Tecentriq, and Bavencio), the company can get acquired if it demonstrates the strong clinical outcomes.

Asides from entinostat, SNDX-6352 is an interesting molecule that can deliver the long-term growth prospects. With many catalysts powering this firm and the asymmetric rewards to risks signified that the company can be a multibagger investment. The main concern for Syndax is if entinostat and the combo can deliver positive Phase 3 data. Since the most value in this company resides in entinostat, a negative reporting can induce the stock to depreciate by over 80%, and vice versa.

Author��s Notes: We��re honored that you took the time to read our market intelligence. Founded by Dr. Hung Tran, MD, MS, CNPR, (in collaborations with Analyst Vu, and other PhDs), Integrated BioSci Investing (��IBI��) is delivering stellar returns. To name a few, Nektar, Spectrum, Atara, and Kite procured over 324%, 144%, 258%, and 83% profits, respectively. Our secret sauce is extreme due diligence with expert data analysis. The service features a once-weekly exclusive Alpha-Intelligence article, daily analysis/consulting, and model portfolios. Of note, there is an IBI version of this article that is a higher-level intelligence with extensive details, in which we published in advanced and exclusively for our subscribers. And, we invite you to subscribe to our marketplace now to lock in the current price and save money for the future.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Our research articles are best used as starting points in your own due diligence. We are not registered investment advisors and our articles are not construed as professional investment advice. Many new research are requests from private investors of our services (Integrated BioSci Investing and Dr. Tran BioSci), who either paid or donated us to support our efforts (in assisting investors and bioscience innovators to deliver hopes to patients). That aside, I like to inform readers of Seeking Alpha's recent policy change, in which the company implemented the paywall (not only to our articles but to all articles that are published over 10-day). This is in place, as the company is, after all, a business. And, the revenues from ads are not adequate to support the high-quality research that the company is providing. If you are a REAL TIME FOLLOWER, you will be notified immediately of our new research for you to continue to benefit from our due diligence. You can also gain access to all of my old articles and much more by taking the 2-week FREE trial of my marketplace, Integrated BioSci Investing.

Syscoin (CURRENCY:SYS) traded 7.6% lower against the U.S. dollar during the 24 hour period ending at 7:00 AM Eastern on August 2nd. One Syscoin coin can now be bought for approximately $0.13 or 0.00001715 BTC on cryptocurrency exchanges including Trade By Trade, Sistemkoin, Bittylicious and Tux Exchange. Syscoin has a market capitalization of $69.90 million and $751,859.00 worth of Syscoin was traded on exchanges in the last 24 hours. In the last week, Syscoin has traded 22.8% lower against the U.S. dollar.

Syscoin (CURRENCY:SYS) traded 7.6% lower against the U.S. dollar during the 24 hour period ending at 7:00 AM Eastern on August 2nd. One Syscoin coin can now be bought for approximately $0.13 or 0.00001715 BTC on cryptocurrency exchanges including Trade By Trade, Sistemkoin, Bittylicious and Tux Exchange. Syscoin has a market capitalization of $69.90 million and $751,859.00 worth of Syscoin was traded on exchanges in the last 24 hours. In the last week, Syscoin has traded 22.8% lower against the U.S. dollar.

.gif "LifePoint Health logo") Headlines about LifePoint Health (NASDAQ:LPNT) have trended positive this week, Accern reports. The research firm scores the sentiment of press coverage by monitoring more than 20 million news and blog sources. Accern ranks coverage of publicly-traded companies on a scale of -1 to 1, with scores nearest to one being the most favorable. LifePoint Health earned a news impact score of 0.44 on Accern’s scale. Accern also assigned news coverage about the company an impact score of 46.0016583450414 out of 100, meaning that recent press coverage is somewhat unlikely to have an impact on the stock’s share price in the immediate future.

Headlines about LifePoint Health (NASDAQ:LPNT) have trended positive this week, Accern reports. The research firm scores the sentiment of press coverage by monitoring more than 20 million news and blog sources. Accern ranks coverage of publicly-traded companies on a scale of -1 to 1, with scores nearest to one being the most favorable. LifePoint Health earned a news impact score of 0.44 on Accern’s scale. Accern also assigned news coverage about the company an impact score of 46.0016583450414 out of 100, meaning that recent press coverage is somewhat unlikely to have an impact on the stock’s share price in the immediate future.